Sold Out, Part 1

How surging inflation and a severe financial crisis will sink the global economy

Issue #112

I just read Sold Out: How Broken Supply Chains, Surging Inflation, and Political Instability Will Sink the Global Economy by James Rickards, which was published in 2022. It's the eighth book I've read by the author, and I think it's his best (five stars and a Must Read). He is obviously well informed, with the knowledge and technical expertise of an insider, as well as being thoughtful, reasonable and a good writer. The book is divided into two parts: the first about the supply chain (which I'll write about next week) and the second about the role of money (which I'll discuss this week).

Rickards notes that all inflation is a form of theft and that borrowers profit at the expense of lenders. “Since the U.S. government is the biggest borrower in the world, it is also the biggest winner from inflation....the Fed's preference for [supposedly only] 2% inflation is like stealing small amounts from people in the hope that no one will notice.” Not surprisingly, after the unprecedented amount of borrowing by governments since 2008, during 2021 “15 out of 34 advanced economies experienced inflation in excess of 5%, the highest number in more than 20 years.”

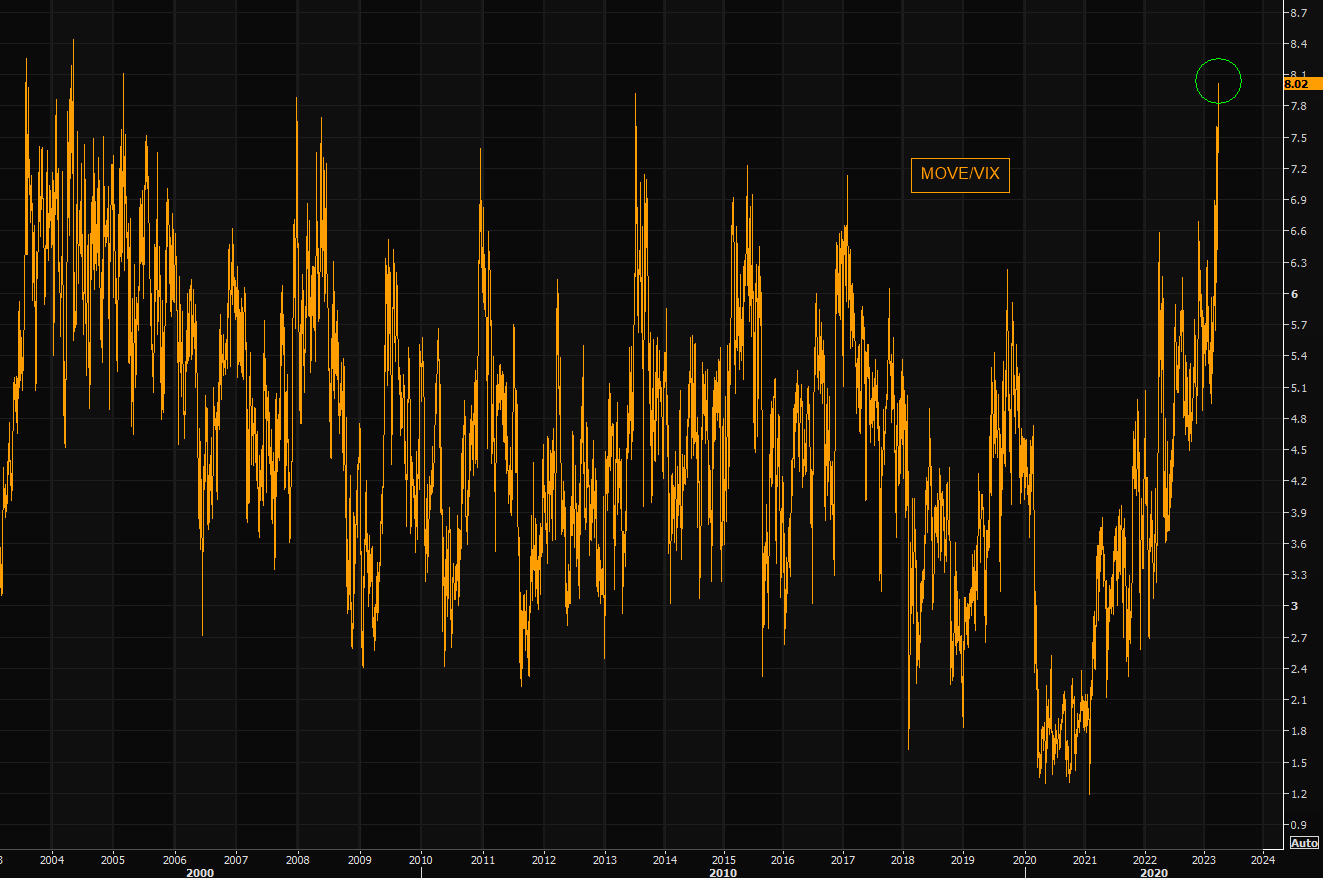

Last week I wrote that First Republic Bank was just a tremor before a mega-financial earthquake. Rickards writes that “...major developments are almost always presaged by clear warnings. [It's best] to put weight on the warnings and not treat them as anomalies.” The bond market (which is larger and generally smarter than the stock market) has already figured this out. The ratio of MOVE (bond market volatility) to VIX (stock market volatility) is near a 20-year high:

Source: Refinitiv

The way that stocks haven't tanked in the last two weeks reminds me of the Phony War in the early days of WWII. Be patient, the Blitzkrieg is coming.

Rickards argues that central banks don't matter because they are impotent to create inflation, so Fed “policy is all for show....What matters are commercial banks in their role as lenders and the appetite of borrowers for new loans....This points to the behavioral root of inflation rather than so-called central bank money printing....Consumer inflationary psychology is most relevant of all. This is why inflation did not emerge when the Fed bloated its balance sheet from 2009 to 2019. It's also why inflation may emerge today despite Fed tightening. The Fed is not in charge.”

Hmm. Well, I don't see mostly insolvent banks wanting (or being able) to lend to borrowers who are tapped out anyway. But it seems that the world (not just Americans, who hold only about half of all dollars) is rapidly losing faith in the dollar. The longer that the real inflation rate remains around 10% or higher, the quicker inflationary psychology will set in among consumers, and the longer it will persist.

Rickards says we could get deflation before hyperinflation. But “economies with high debt-to-GDP ratios often flip from disinflation (or deflation) to hyperinflation almost overnight as citizens and creditors suddenly realize that inflation is the only way to escape the room....In the long run, [high debt levels] are almost certainly inflationary. The phase transition from one state to the other will be both unexpected and sudden....the timing is unclear, but the outcome is certain.” The phase transition occurs when suddenly, the truth becomes apparent to almost everyone, and they radically change their behavior all at once. It is difficult to envision a phase transition until it occurs.

Rickards explains why the human race is dying out due to collapsing birth rates in most countries, and how that will lead to slower economic growth and higher labor costs. The replacement ratio needed to maintain a population at the current level (2.1) is well below that in Japan (1.4), Europe and Brazil (1.5), and the U.S., China and Australia (1.7). The world is becoming a heavily indebted nursing home, leaving fewer younger people to work and pay taxes.

One book I have (after shelling out $40 for) but haven't read yet is The Seneca Effect: Why Growth Is Slow But Collapse Is Rapid. Rickards writes, “The tempo of bubbles inflating and bursting is asymmetric. The expanding phase lasts for years or even decades. The collapse comes in weeks or months....” Recency bias also makes collapse difficult to imagine.

Rickards predicts the Fed will break something by committing a policy error (in the current case, hiking interest rates in the face of obvious economic weakness): “All the forecaster has to do is listen to the Fed, believe it, and then make allowance for its inevitable failure. The forecast will be accurate for a year or more as the Fed stumbles down the wrong path. The challenge is to estimate the point at which even the Fed must bow to reality. For that eventuality you look to market signals, particularly in the bond market [see chart above] and the Eurodollar futures curve. [They] will validate the fact that the Fed is headed over a cliff. The Fed will be the last to know....The only issue is how much damage is done before it wakes up.”

Rickards continues: “...the Fed will persist in following its announced policies despite market warnings that it is on the wrong path.” Why does the Fed do this? Well, humans have a strong desire to appear to be consistent, a quality that must have been valued by the tribe. Additionally, Rickards notes that the Fed used to be “both more humble about the fact that errors occur and more circumspect in announcing its policies in the first place.” Now it acts more like the Oracle of Delphi (investors and the financial media certainly treat it that way, breathlessly awaiting its pronouncements from Mount Eccles) by predicting the future with its economic projections and dot plots.

The theoretical justification for having a central bank determine interest rates and the money supply is that a highly educated, enlightened and benevolent elite know better how to do that than the forces of supply and demand on the market. (Apparently, the market works OK for pricing say gasoline, but not for pricing money.) So the Fed has to don the robes and play the role of the oracle even though in reality, they have no idea what they're doing.

What hath the Fed's ultra-low interest rates since at least 2002 wrought? “...the U.S. and the world are in the midst of four simultaneous superbubbles [real estate, stocks, bonds and commodities] constituting the most dangerous financial condition ever recorded.... Housing prices...are the highest multiple of family income ever recorded....Stock prices are at all-time highs or near highs using multiple metrics, including P/E ratios, the ratio of total stock market capitalization to GDP (the Buffett Indicator), and the Shiller CAPE ratio. The stock/GDP ratio (using the Wilshire 5000) in February 2022 was 189.8. This compares to a ratio of 105.3 prior to the 2008 global financial crisis, and 140.7 prior to the 2000 dot.com crash. The Shiller CAPE ratio in February 2022 was 36.2 compared to a 150-year mean ratio of 16.9 and median ratio of 15.9. That ratio is higher than the 1929 peak of 30, and second only to the 2000 dot.com peak of 44.2.”

Rickards explains how an opaque market you've probably never heard of could trigger or greatly magnify a global financial crisis: “The real engine of global finance, trade and investment is a kind of shadow money created by banks outside the purview of central banks and scarcely regulated or even understood by regulators—Eurodollars. These are loans and deposits made by banks to each other and to large corporations, denominated in U.S. dollars but created in...offshore banking centers around the world not subject to direct banking regulation or reporting. Eurodollar deposits can be used to buy high-quality securities, which are then pledged to other banks for more cash used to buy more securities, which are also pledged, and so on until a vast pyramid of unregulated dollars, pledged securities, and extreme leverage exists....”

But wait, it gets better: “...another even larger pyramid is placed on top of the Eurodollar pile in the form of derivatives, basically side bets on the underlying positions on the bank's books. These derivative side bets are not only unregulated, they are invisible. They exist in opaque financial statement footnotes as aggregate notional values, but do not appear on the financial statements themselves and are not disclosed with more than cursory details. There is no limit on the notional value of derivatives that may be created in relation to a given value in an underlying position. A $1 billion derivative position can be layered on top of a $1 million securities position, bearing in mind the $1 million securities position might be supported by as little as $5,000 in cash...with the remaining $995,000 consisting of pledged securities in the form of repos.”

And now for the punchline: “The key to this impossibly leveraged Eurodollar world is collateral. If you're supporting a $1 million position with $5,000 in cash and $995,000 in collateral, then that collateral better be the safest, most liquid security in the world. A minute market move against the leveraged trader will wipe out the cash position in an instant....Likewise, the much larger derivatives trade has its own margin requirements that must be satisfied by the trader with high-quality collateral if the position loses money. From the lender's perspective, it's bad enough if the counterparty is losing money on the trade...but matters get worse if the collateral itself loses value, compounding the trading loss and credit default....there is one and only one type of collateral that satisfies the lender's requirements for liquidity, creditworthiness, and low volatility—short-term U.S. Treasury bills.” Hmm, what could go wrong with this? What happens to this collateral when investors realize that the dollar is being rapidly debased and the federal government's debt can never be repaid?

“Research offers concrete empirical signs that can warn investors if a global dollar shortage and associated Treasury bill shortage are emerging. It is a kind of early warning of another global financial collapse. The first sign is a flattening of the U.S. Treasury yield curve....This implies that markets do not see robust growth or inflation ahead; they see the opposite. The extreme form of this is an inverted yield curve, where long-term rates are lower than short-term rates [which is currently the case]. That's a bright flashing red light almost always associated with a recession or worse.”

Rickards predicts, “At the crisis stage, the Fed will activate dollar swap lines with selected foreign central banks to provide dollars to those central banks so they can bail out their own banks, which can no longer access dollars in interbank markets.” That's exactly what happened less than two weeks ago.

Rickards concludes by noting that the government policy of fiscal dominance (which is “pursuing slow, steady inflation that whittles away the real value of the debt without causing panic or changing the behavior of everyday consumers”) depends on the money illusion (which is “the phenomenon that citizens do not recognize low-level inflation even though it steals purchasing power by the day”). The danger of this “is that some exogenous event bursts the bubble of money illusion, and behavior shifts suddenly to demand-pull inflation as consumers spend more to beat price increases and workers demand raises to preserve purchasing power....The money illusion was gone once prices at the [gas] pump tripled [in the late 1970s]. That could happen again if modern monetary theory, which supports unlimited deficits and unlimited money printing, lasts much longer.” So what would proponents of Modern Monetary Theory do about surging inflation? Would they cut government spending? No, they would reduce deficits by raising taxes.

Leviathan can never be satisfied. Its maw will always remain wide open, gorging itself on stolen wealth by any means necessary (inflation, taxes, confiscation) until there is nothing of value left, at which point it will collapse like a dying star. The government (and the 1% elite who control it) are coming for your wealth. We are in the early hyperinflationary stage now. Next will come high taxes and heavy-handed enforcement. Once the dollar collapses, the final phase will be outright physical confiscation. Get prepared now.

News Items

Buy/Rent Premium Highest Since 2006 Housing Bubble Peak

Two Merrill Traders Sentenced to Prison for Manipulating Precious Metals Prices

Perth Mint Sold Diluted Gold to China, Got Caught, Tried to Cover It Up

I would love to hear from you! If you have any comments, suggestions, insight/wisdom, or you'd like to share a great article, please leave a comment.

Disclaimer

The content of this newsletter is intended to be and should be used for informational/ educational purposes only. You should not assume that it is accurate or that following my recommendations will produce a positive result for you. You should either do your own research and analysis, or hire a qualified professional who is aware of the facts and circumstances of your individual situation.

Financial Preparedness LLC is not a registered investment advisor. I am not an attorney, accountant, doctor, nutritionist or psychologist. I am not YOUR financial planner or investment advisor, and you are not my client.

Investments carry risk, are not guaranteed, and do fluctuate in value, and you can lose your entire investment. Past performance is not indicative of future performance. You should not invest in something you don't understand, or put all of your eggs in one basket.

Before starting a new diet or exercise regimen, you should consult with a doctor, nutritionist, dietician, or personal trainer.

Thanks Rob, great info

Clardy